The Indian government is reportedly considering taking “the ordinance route” to quickly pass the cryptocurrency bill. “The government is of the firm view that they want to introduce the law within a month of clearance of the ordinance,” a local news outlet detailed.

Indian Government Seeks to Quickly Pass Crypto Bill

All eyes are on what the government of India will do with the cryptocurrency bill that is listed to be introduced in the current session of parliament. The bill seeks to ban cryptocurrencies while creating a framework for the official digital currency to be issued by the central bank, the Reserve Bank of India (RBI).

On Friday, CNBC-TV18 reported that “The government may take the ordinance route to pass the Cryptocurrency and Regulation of Official Digital Currency Bill,” citing unnamed sources. The news outlet elaborated:

The PMO, Finance Ministry, and Cabinet

The PMO, Finance Ministry, and Cabinet Secretariat have started preparing the draft details of the ordinance. The government is of the firm view that they want to introduce the law within a month of clearance of the ordinance

“They want this bill to be cleared as soon as possible,” reporter Timsy Jaipuria noted. She added that “the cabinet is understood to have given clearance to this particular proposal that this bill can be introduced via an ordinance route in its last meeting which was held on Feb. 3.”

Ordinances are promulgated by the president of India on the recommendation of the Union Cabinet. They have the same effect as an Act of Parliament. Ordinances can only be issued when Parliament is not in session, enabling the government to take immediate legislative action. The current Budget session began on Jan. 29 and will end on April 8. It is held in two phases; the first phase will end on Feb. 13 and the second will start on March 8.

The cryptocurrency bill could resemble the one drafted by an interministerial committee (IMC) headed by former Finance Secretary Subhash Chandra Garg, who has now resigned from the government. Recently, the Minister of State for Finance Anurag Thakur answered some crypto questions in Rajya Sabha, the upper house of India’s parliament, clarifying the government’s stance on cryptocurrency and the digital rupee.

There are still many unanswered questions about the bill the government is planning to introduce and many are just waiting for the bill to become public. Meanwhile, the Indian crypto industry has launched a campaign to convince the government not to impose a ban on cryptocurrencies.

Indian cryptocurrency exchanges have started a joint initiative to convince parliament to regulate cryptocurrencies rather than impose an outright ban.

Under the IndiaWantsBitcoin campaign, the exchanges have launched websites – indiawantscrypto.net and indiawantsbitcoin.org – to help Indian citizens email their representatives at the Loksabha (the lower house of parliament) asking for positive and progressive regulation of the crypto markets.

The campaign has been launched in response to the government’s plan to table the “Cryptocurrency and Regulation of Official Digital Currency Bill 2021,” which would potentially prompt development of a digital rupee while banning “private cryptocurrencies.” While exactly what the bill means for cryptocurrencies like bitcoin and ether isn’t clear, but the industry has concerns.

The campaign is being shared across social media, with supporters tagging friends and urging them to do their bit.

“Within one day, over 10,000 emails have been sent via indiawantscrypto.net from all parts of the country,” Nischal Shetty, CEO of the Binance-owned WazirX exchange, told CoinDesk. “It’s a critical moment, and all eyes are on India to find out if we’re for or against innovation.”

The five email templates available on both websites highlight the positive role cryptocurrencies can play in helping Prime Minister Narendra Modi achieve his aim of a “digital India” and “atmanirbhar bharat” (self-reliant India).

“I am concerned that the prohibition of private cryptocurrencies might stun the growth of Digital India. With the world embracing cryptocurrencies, it would be regressive for India to be deprived of such once in a generation opportunity,” one email template says.

Another says a potential ban would significantly affect the ecosystem, comprising 10-20 million cryptocurrency users, 340 startups providing related services and direct employment to 50,000 Indians.

The Indian crypto industry has witnessed solid growth since the Supreme Court overruled the Reserve Bank of India’s banking ban on cryptocurrency firms in March 2020.

As per the recent data from Venture Intelligence, investments worth a whopping $24 million have gone into various crypto firms from India in the year 2020,” Sumit Gupta, CEO of the Mumbai-based CoinDCX exchange, told CoinDesk.

As such, a potential ban may result in a significant economic damage for the world’s second-most populous country, as well as have a negative effect on the cryptocurrency markets.

However, an Indian minister recently hinted any ban may be limited, stating that the government aims to curb illicit cryptocurrency transactions and bar their use in payments.

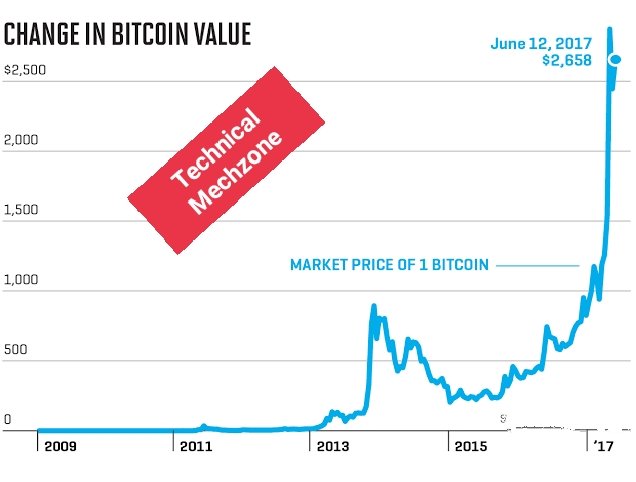

The wild swings in the price of Bitcoin prove it’s not a real unit of value, though blockchain technology “is here to stay,” according to Goldman Sachs Group Inc.’s Sharmin Mossavar-Rahmani.

Something with a long-term volatility of 80% can’t be considered a medium of exchange,” said Rahmani, head of the investment-strategy group for the bank’s consumer and investment-management division. Just because everybody piles into into an idea and talks it up doesn’t mean it’s a store of value,” she said during a briefing Wednesday on the group’s 2021 outlook, comparing the cryptocurrency’s spikes to the recent run-up in GameStop Corp.

Bitcoin surged to a record close of almost $41,000 in early January, but has since dropped back to about $37,000.

Rahmani’s skepticism about Bitcoin’s intrinsic value echoes that of European Central Bank governing council member Gabriel Makhlouf, who said last month Bitcoin investors should be prepared to “lose all their money.” Still, the cryptocurrency has plenty of high-profile proponents.

Paul Tudor Jones bought some as a hedge against central bank and government action, while Mike Novogratz and Alan Howard have both invested hundreds of millions of dollars in Bitcoin and other digital currencies. Bridgewater Associates founder Ray Dalio has called it “one hell of an invention” and an alternative, gold-like asset. Rahmani drew a distinction between Bitcoin and blockchain technology, the public, mostly anonymous ledger that records all the currency’s transactions. That technology could facilitate the smoother flow of global assets and will become part of the financial infrastructure, she said.

Despite doubters on Wall Street, the unceasing buzz over Bitcoin is leading more banks to develop cryptocurrency products for clients. JPMorgan Chase & Co. launched its own digital currency last year and Fidelity Investments started a Bitcoin-only fund. Even Goldman Sachs may be joining the party. The bank issued a request for information to at least one crypto custody player at the end of 2020, website CoinDesk reported in January.

Mostly cement stocks have gained substantially in the last two trading sessions and Ambaja Cement is also trading in tandem with the trend. It surged almost vertically from the support zone of the medium-term moving average (100 EMA) on the daily chart and made a new record high as well. The chart pattern, combined with recent buoyancy in the market, is pointing towards a steady up move ahead. Traders can create fresh longs on any dip in the given range.

MothersonSumi Systems Limited Recommendation: Buy Last Close: 156.30 Initiation range: 156-158 Target: 180 Stop loss: 145

MothersonSumi has retraced marginally and tested the support zone around 140, taking a breather after a strong recovery from the March 2020 lows. It has formed a fresh buying pivot now and looks all set to resume the uptrend. We thus advise creating fresh longs in the mentioned zone.

Zee Entertainment Enterprises Limited Recommendation: Buy Last Close: 242.90 Initiation range: 240-242 Target: 260 Stop loss: 228

We’re seeing a gradual recovery in media stocks and Zee Entertainment is also participating in the move now. It has witnessed a fresh breakout on February 2, after spending nearly one and a half months in a consolidation range. Indications are in the favour of recent momentum to extend further. Traders shouldn’t miss this opportunity and create fresh longs in the given range.

Note: Dear readers

Business Standard has always strived hard to provide up-to-date information and commentary on developments that are of interest to you and have wider political and economic implications for the country and the world. Your encouragement and constant feedback on how to improve our offering have only made our resolve and commitment to these ideals stronger. Even during these difficult times arising out of Covid-19, we continue to remain committed to keeping you informed and updated with credible news, authoritative views and incisive commentary on topical issues of relevance.

• The government’s plan to ban all private cryptocurrencies in India has spooked investors with prices of the world’s oldest cryptocurrency bitcoin trading at a steep discount of up to 20% against a premium of 10% in the last few days.

The government on Friday had listed a bill, which proposes to ban all private cryptocurrencies in India — such as bitcoin, ether, ripple — in the legislative order of business for the Budget Session of 17th Lok Sabha. The Cryptocurrency and Regulation of Official Digital Currency Bill, 2021 also stated that certain exceptions to promote the underlying technology of cryptocurrency and its uses would be allowed.

Due to the fact that a cryptocurrency draft bill leading to its ban has got listed in the items for discussion during this budget session, the entire industry is in panic. We have seen some panic selling as well, which has led to reduced prices of cryptocurrencies. Bitcoin and ether, which used to trade at 10% premium compared with global markets are now trading at 20% discount,” said Sathvik Vishwanath, co-founder and chief executive officer, Unocoin. *According to the expert, cryptocurrencies didn’t see any notable recovery despite the topic not coming up in the budget speech. Bitcoin was trading marginally higher on Tuesday after hitting a high and a low of $34,715.66 and $33,150.73, respectively, over the past 24 hours The government’s plan to ban all private cryptocurrencies in India has spooked investors with prices of the world’s oldest cryptocurrency bitcoin trading at a steep discount of up to 20% against a premium of 10% in the last few days.

The government on Friday had listed a bill, which proposes to ban all private cryptocurrencies in India — such as bitcoin, ether, ripple — in the legislative order of business for the Budget Session of 17th Lok Sabha.

The Cryptocurrency and Regulation of Official Digital Currency Bill, 2021 also stated that certain exceptions to promote the underlying technology of cryptocurrency and its uses would be allowed.

“Due to the fact that a cryptocurrency draft bill leading to its ban has got listed in the items for discussion during this budget session, the entire industry is in panic. We have seen some panic selling as well, which has led to reduced prices of cryptocurrencies. Bitcoin and ether, which used to trade at 10% premium compared with global markets are now trading at 20% discount,” said Sathvik Vishwanath, co-founder and chief executive officer, Unocoin.

According to the expert, cryptocurrencies didn’t see any notable recovery despite the topic not coming up in the budget speech.

Bitcoin was trading marginally higher on Tuesday after hitting a high and a low of $34,715.66 and $33,150.73, respectively, over the past 24 hours. It was trading at $34,265 at 1.45 pm (IST) on Tuesday, as per data available with crypto exchange WazirX.

Last year, the Supreme Court of India had quashed a Reserve Bank of India’s (RBI) ban on crypto-related payments.

Industry experts also are hoping for government support. “The contents of the draft bill remain unknown, which is also adding to the panic of the community. India is known for following the footsteps of developed counties when it comes to technical innovation and it is the time for governments and regulators to look at how this has played out there more closely before making knee-jerk reactions,” said Vishwanath.

RBI earlier had also said that the apex bank is exploring a digital version of the rupee.

“We’re proud that the RBI is exploring a digital rupee built on a blockchain. Blockchain technology not only lowers costs, but it also improves accounting since it is an immutable ledger, which would give the government new tools to fight corruption. However, creating a government currency doesn’t require the banning of non-government crypto assets. On the contrary, safely including all aspects of this new technology will bring tremendous tax revenue and innovation,” said Rahul Pagidipati, chief executive officer at ZebPay.

In other cryptocurrencies, ethereum and tether were trading in the green by up to 8%, while stellar was down 5% in the red on Tuesday.

Crypto firms in India have also experienced a successful year since the lockdowns in March 2020. Trading on crypto exchanges increased manifold, while Bitcoin’s sudden bull run in December brought in more investors as well. The current move poses a threat to the future of this industry

NEW DELHI: The domestic cryptocurrency industry has been urging the Center to reconsider its apparent plan to ban private cryptocurrencies, like Bitcoin, in India. Industry stakeholders said while the government’s intention to create a Central Bank Digital Currency (CBDC) is a welcome move, the definition of what the government considers “private cryptocurrencies” will be important.

The Indian government’s plan to “create a facilitative framework for creation of the official digital currency to be issued by the Reserve Bank of India (RBI),” was announced in the agenda for the upcoming Budget session of Parliament. The legislation seeks “to prohibit all private cryptocurrencies in India”, the agenda said. It is meant to allow the use of blockchain technology, which is the underlying tech behind cryptocurrencies, but many expect that it will make the use of currencies like Bitcoin and Ethereum illegal in the country.

“The digital currency bill to be introduced in the Lok Sabha is a welcome step. Its success will depend on the details, particularly the definition of what the bill calls ‘private cryptocurrencies’. This is not a common term. Bitcoin is not privately owned by anyone. It is a public good, like the internet,” said Rahul Pagdipati, chief executive officer (CEO) of crypto exchange and wallet ZebPay.

Industry executives say the government’s concern is likely about the possible use of cryptocurrency as an alternative to the Indian rupee (INR). They argued that cryptocurrencies instead are similar to assets such as gold. “As an industry, we’re in sync with the fact that INR is the only legal tender in India and about crypto being an asset/utility that people buy and sell,” said Nishcal Shetty, founder of WazirX, India’s largest cryptocurrency exchange, which was acquired by Binance, the largest crypto exchange in the world.

“Bitcoin and most crypto assets are more like gold and not an alternative to government-issued legal tender,” said Pagdipati. “Crypto assets and digital government currency can coexist and together,” he said.

The industry has urged the government to consult stakeholders before coming to a decision. “We urge the government to take the opinion of all the stakeholders before taking a decision that may affect the livelihood of the entire workforce employed in the digital asset industry in India,” said Shivram Thukral, CEO of BuyUcoin, another cryptocurrency exchange and wallet. “We have faith in the government and hope that this bill will move India forwards, not backwards,” said Pagdipati The latest declines are occurring almost a year after cryptocurrency markets, fuelled by a rush of new, wealthy investors, went into overdrive. Crypto firms in India have also experienced a successful year since the lockdowns in March 2020. Trading on crypto exchanges increased manifold, while Bitcoin’s sudden bull run in December brought in more investors as well. The current move poses a threat to the future of this industry

NEW DELHI: The domestic cryptocurrency industry has been urging the Center to reconsider its apparent plan to ban private cryptocurrencies, like Bitcoin, in India. Industry stakeholders said while the government’s intention to create a Central Bank Digital Currency (CBDC) is a welcome move, the definition of what the government considers “private cryptocurrencies” will be important.

The Indian government’s plan to “create a facilitative framework for creation of the official digital currency to be issued by the Reserve Bank of India (RBI),” was announced in the agenda for the upcoming Budget session of Parliament. The legislation seeks “to prohibit all private cryptocurrencies in India”, the agenda said. It is meant to allow the use of blockchain technology, which is the underlying tech behind cryptocurrencies, but many expect that it will make the use of currencies like Bitcoin and Ethereum illegal in the country.

“The digital currency bill to be introduced in the Lok Sabha is a welcome step. Its success will depend on the details, particularly the definition of what the bill calls ‘private cryptocurrencies’. This is not a common term. Bitcoin is not privately owned by anyone. It is a public good, like the internet,” said Rahul Pagdipati, chief executive officer (CEO) of crypto exchange and wallet ZebPay.

Industry executives say the government’s concern is likely about the possible use of cryptocurrency as an alternative to the Indian rupee (INR). They argued that cryptocurrencies instead are similar to assets such as gold. “As an industry, we’re in sync with the fact that INR is the only legal tender in India and about crypto being an asset/utility that people buy and sell,” said Nishcal Shetty, founder of WazirX, India’s largest cryptocurrency exchange, which was acquired by Binance, the largest crypto exchange in the world.

“Bitcoin and most crypto assets are more like gold and not an alternative to government-issued legal tender,” said Pagdipati. “Crypto assets and digital government currency can coexist and together,” he said.

The industry has urged the government to consult stakeholders before coming to a decision. “We urge the government to take the opinion of all the stakeholders before taking a decision that may affect the livelihood of the entire workforce employed in the digital asset industry in India,” said Shivram Thukral, CEO of BuyUcoin, another cryptocurrency exchange and wallet. “We have faith in the government and hope that this bill will move India forwards, not backwards,” said Pagdipati.

India has considered banning cryptocurrencies once earlier. The government had floated a draft bill for “Banning of Cryptocurrency and Regulation of Official Digital Currency Bill” in 2019. That bill proposed a fine or imprisonment of up to 10 years, or both, for mining, holding, selling, trade, issuance, disposal or use of crypto in India. The Reserve Bank of India (RBI) had also issued a circular in 2019 that banned banks and other regulated entities from doing business with crypto companies. This was struck down by the Supreme Court last year.

According to data from analysis firm Venture Intelligence, investments worth $24 million went into crypto firms in 2020, after the Supreme Court’s decision, up from a mere $5 million in the year before. Crypto firms in India have also experienced a successful year since the lockdowns in March 2020. Trading on crypto exchanges increased manifold, while Bitcoin’s sudden bull run in December brought in more investors too. The government’s current move threatens to put the future of this industry in disarray once again.

For those interested in cryptocurrencies, the government of India has listed a bill to be introduced in the Parliament during the Budget session of the 17th Lok Sabha. The bill seeks to ban private cryptocurrencies like Bitcoin, Ripple, Ether, and others in India.

The government is likely to table the Cryptocurrency and Regulation of Official Digital Currency Bill, 2021. It is aimed at creating a ‘facilitative framework’ for an official digital currency in India to be issued by the banking regulator, the Reserve Bank of India (RBI). The government’s bill also seeks to ban the Bitcoin, Ether, Ripple, and other private cryptocurrencies but it may allow certain kinds of uses and promotions of the technology behind them.

According to the RBI booklet on payment systems, the government is sceptical of these currencies and RBI is exploring the creation of a digital version of the Indian national currency.

“In India, the regulators and governments have been sceptical about these currencies and are apprehensive about the associated risks. Nevertheless, RBI is exploring the possibility as to whether there is a need for a digital version of fiat currency and, in case there is, how to operationalise it,” the booklet said while acknowledging how private digital currencies have gained popularity recently. These private cryptocurrencies were banned earlier as well, but the Supreme Court later overturned the previous ban in 2018.

It is to be noted that the government is considering the introduction of a bill to set up a development finance institution (DFI) in India as well. The central government will introduce The National Bank for Financing Infrastructure and Development (NaBFID) Bill, 2021 in the Parliament.

According to media reports, the DFI is going to act as a catalyst and promote infrastructural financing. It will be the principal financial institution and development bank in India to provide a supportive ecosystem for the infrastructure projects in the country across their life-cycle. Posted by Technical Mechzone

The budget session of Parliament is all set to introduce a new bill that bans private cryptocurrencies and provides for an official digital currency to be issued by the Reserve Bank of India.

The Union Budget, which will be presented on February 1, is looking towards the introduction, consideration, and passing of the Cryptocurrency and Regulation of Official Digital Currency Bill. Apart from prohibiting all private cryptocurrencies in India, the bill also seeks to create a facilitative framework for an official digital currency issued by the RBI. However, as per a Lok Sabha bulletin, the bill allows for certain exceptions to promote the underlying technology of cryptocurrency and its uses. In 2018, the Indian central bank had banned crypto transactions after a number of frauds came to the fore following PM Modi’s decision to ban 80% of the nation’s currency. As a result, the Cryptocurrency trade was brought to a halt after the RBI asked all regulated entities, such as banks, to stop any dealings related to private cryptocurrencies as part of that order.However, the table’s turned when a supreme court bench, headed by Justice Rohinton F Nariman, quashed the central bank’s circular on grounds of disproportionality.

According to a report by Bloomberg, the court ruled that RBI had failed to show “at least some semblance of any damage suffered by its regulated entities’’ to back its decision to effectively bar cryptocurrencies in India.” From then Cryptocurrency exchanges began operations yet again.

The rapid surge in the price of Bitcoins accelerated its use by top banks, which had stopped dealing with cryptocurrency exchanges after the RBI’s order. The dealings with the cryptocurrency became a point of global debate. Large Investment houses said that Bitcoins can be seen as an alternative to gold. JPMorgan said that “a crowding out of gold as an ‘alternative’ currency implies big upside for bitcoin over the long term.” Earlier this week, Bridgewater Associates founder Ray Dalio said Bitcoin is “one hell of an invention” and added that he is considering cryptocurrencies as investments for new funds offering clients protection against the debasement of fiat money. To further this cause, payment networks such as Paypal, MasterCard, and Visa also moved to set up systems that accept payments via cryptocurrencies.

Also, this week, the RBI had reiterated that it was exploring the need for a digital version of the fiat currency.

(An RBI booklet on payment systems issued on 25th Jan also showed that the central bank is exploring whether to issue a digital version of the rupee)

In the legislative order of business for the budget session of 17th Lok Sabha that commenced today, the Government has listed a bill providing for the banning of all private cryptocurrencies in India such as bitcoin, ether, ripple and others. The bill also provides for the creation of a legislative framework on an official digital currency.

An RBI booklet on payment systems issued on 25th Jan also showed that the central bank is exploring whether to issue a digital version of the rupee. “Private digital currencies have gained popularity in recent years,” the central bank booklet said. “In India, the regulators and governments have been sceptical about these currencies and are apprehensive about the associated risks.

Nevertheless, RBI is exploring the possibility as to whether there is a need for a digital version of fiat currency and, in case there is, how to operationalize it,” it noted. A previous RBI ban on the use of bank channels for payments associated with cryptocurrency issued in 2018 was overturned by the Supreme Court in March 2020 creating a vacuum in the regulation of cryptocurrency in India. Posted by Technical Mechzone

Led by losses in index heavyweight Reliance Industries, private lenders and select IT stocks, benchmark indices extended their losses to the fourth day on Wednesday. Weak global markets, a mixed set of Q3 earnings and selling by foreign institutional investors (FIIs) dented the domestic market mood in today’s session. Meanwhile, investors chose to book profits ahead of the Union Budget on Monday, February 1. The BSE barometer Sensex plunged 938 points to 47,410 while its NSE counterpart Nifty slipped below the 14,000 mark to end at 13,968, down 271 points.

The broader market trend was mixed with Nifty Midcap 100 and Nifty 500 indices down 1.58 per cent and 1.68 per cent, respectively, while Nifty Smallcap index added 0.15 per cent. The volatility also remained high ahead of the monthly F&O expiry on Thursday, with India VIX rising 4.93 per cent to 24.39 level. Here are the top factors behind the market crash today. Weak global cues

Asian equities slipped on Wednesday as investors looked to the Federal Reserve’s guidance on its monetary policy while futures for US tech shares jumped after strong earnings from Microsoft. European stocks are expected to slip a tad, with EuroStoxx 50 futures down 0.3 per cent and FTSE futures shedding 0.4 per cent. Global stocks are mostly treading water near record highs as US corporate earnings roll in. Meanwhile, new coronavirus variants that sparked fresh lockdowns and other restrictions are weighing on the market mood.

Frustration over vaccine distribution is also increasing. In a Facebook post last week, Italian Prime Minister described delays in consignments by Pfizer Inc. and AstraZeneca Plc as “unacceptable” while the UK’s health minister warned that vaccines may be less effective against new variants of the coronavirus. That apart, investors are also seeking more clarity on the timeline for President Joe Biden’s $1.9 trillion Covid-19 relief plan. “Delay in US paycheques and overall correction in global markets are driving indices lower. Liquidity is a critical factor right now and any fall in liquidity will lead to a sharp fall in markets,” said Abhimanyu Sofat, Head of Research at IIFL Securities. Budget blues

The Union Budget, set to be unveiled on February 1, is a highly anticipated affair as it comes on the heels of a pandemic that has altered India’s economic landscape. Amid this backdrop, investors have booked profits and are waiting on the sidelines. The government needs to raise resources to help increase spends, but analysts at Bernstein believe equity markets will consider any form of tax increases negative. Those at Credit Suisse, on the other hand, caution against the limited spending room the government has. “While the government appears to be willing to spend now, as it believes the growth multiplier would be higher in an economy without Covid-19 restrictions, Rs 4.2 trillion of extra spending may be difficult to execute. It may choose to be conservative on GDP growth assumptions, and also target a lower deficit, which would imply 13 per cent total expenditure growth. In this scenario, spending on residual heads could be 40% higher than in FY20, but the absolute increase a more reasonable Rs 2.5 trillion,” wrote Neelkanth Mishra, managing director, co-head of Asia Pacific Strategy and India equity strategist at Credit Suisse in a recent report co-authored with Abhay Khaitan and Prateek Singh.

Q3 earnings In the December quarter earnings season, the companies have posted a robust performance but this was mostly pencilled in by the market. However, a performance by Reliance Industries disappointed investors, leading to a massive fall in the company’s shares and subsequently the benchmark indices. Going ahead, analysts are concerned about lower margins. “We are lowering in expectations for forthcoming quarters on margin front as they are expected to peak out in the current quarter,” said Sofat. Valuation concerns The market is overvalued from the perspective of PE multiple and market-cap to GDP ratio. The overvaluation is more than 50 percentage points higher than the historical average. “Profit-booking is normal, particularly when valuations are high, like now,” said Vijay Kumar, adding that such profit-taking is healthy and desirable.

For the third consecutive session on Monday, Nifty50 formed a Long Bear Candle. “The three sessions consecutive decline was formed in the market after the time span of four months. Hence, this pattern could be in-line with the reversal formation in the market at the highs. The last swing high of 14,753 of January 21 could be a reversal high for the near-term,” said Nagaraj Shetti, Technical Research Analyst at HDFC Securities in a note on January 25. Nifty on the weekly chart, formed a Doji and high wave-type candlestick pattern back to back in the last two weeks, Jasani said, adding that this market action could be considered as a beginning of major profit booking in the market from the high.